Estate Planning

Assets for Revocable Trusts in New York

Assets That Can and Cannot Go Into Revocable Trusts Introduction to Revocable Trusts Revocable trusts are a cornerstone of estate planning in New York, offering

Assets That Can and Cannot Go Into Revocable Trusts Introduction to Revocable Trusts Revocable trusts are a cornerstone of estate planning in New York, offering

Understanding Trusts and Wills in New York: Essential Tools for Estate Planning Planning for the future requires careful attention to detail, especially when it involves

Understanding the Totten Trust in New York In the complex world of estate planning, the Totten Trust often stands out as a unique and straightforward

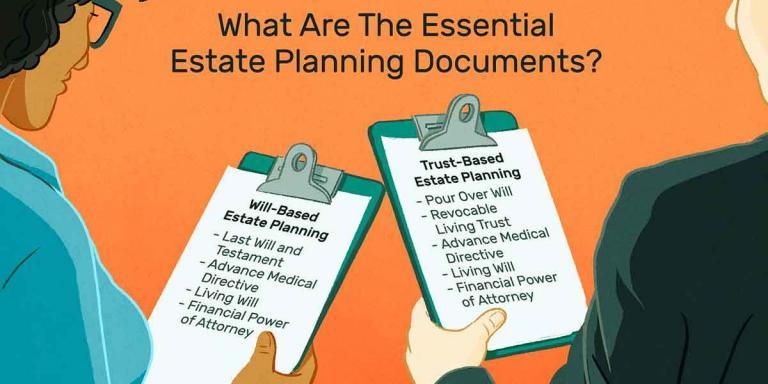

All About Revocable Trusts in New York To ensure your assets are managed and distributed according to your wishes, estate planning is essential. One of

Assets to Put in a Revocable Living Trust in New York At Morgan Legal Group, located in New York City, we specialize in estate planning,

Understanding the Basics of a Revocable Trust At Morgan Legal Group, located in New York City, we specialize in estate planning, probate, elder law, wills,

Revocable Trusts Vs. Irrevocable Trusts A revocable trust is a proficient method of appropriating resources. It accompanies a gathering of advantages that the grantor and

What Is A Living Revocable Trust To get what a revocable living trust is, how about we separate the term. Revocable implies that the trust

Living Revocable Trusts Can; – 1 These living trusts help you stay away from probate. Probate has a terrible standing. It’s an interaction when an

Now you have created your revocable trust, you look forward to avoiding or minimizing probate. But now the big deal is to determine what assets