How to Minimize Estate Taxes and Probate Costs in New York (2026 Guide)

When a loved one passes away, families often face an overwhelming combination of emotional grief and sudden financial complexity. As assets move through the legal system, executors and beneficiaries frequently ask a critical question: “How can we minimize inheritance tax during the probate process?” For residents of New York City, understanding the exact rules of taxation is vital to saving the family legacy from catastrophic losses.

First, we must clarify a fundamental legal distinction under New York State law. New York does not impose an “inheritance tax,” which would be a tax paid directly by the person receiving the property. Instead, New York enforces a strict and aggressive **estate tax**. This tax targets the total value of the deceased person’s property before any distributions reach the heirs. When an estate undergoes the formal probate process, minimizing this financial burden becomes the top priority for the executor.

I am Russel Morgan, the managing attorney of Morgan Legal Group. Over the course of handling more than 1,000 successful cases and earning 900+ positive online reviews, I have seen the devastating impact of unoptimized planning. In 2026, saving an estate from the New York tax collector requires deep tactical execution. This comprehensive cornerstone guide outlines the precise steps an executor can take during probate, and the proactive measures individuals must establish today to shield their wealth.

The Ultimate Threat: The New York Estate Tax “Cliff”

To effectively protect your family assets during the estate planning consultation NYC process or a live probate proceeding, you must comprehend how New York calculates its estate tax. New York is one of the few states in the country that utilizes a tax mechanism known as the “cliff.”

Understanding the Cliff Mechanics

In 2026, the New York State estate tax exemption threshold is highly specific. If the total taxable value of an estate remains below this state-mandated limit, the estate owes zero dollars to Albany. However, if the value of your estate exceeds that exemption threshold by a mere 5%, the entire exemption is completely wiped out. The state then levies taxes on the **entire estate** starting from dollar number one. The tax rates quickly escalate from 3.06% up to 16%.

The Financial Fallout

This means that going even a single dollar over the 105% buffer line can instantly cost a family hundreds of thousands of dollars in avoidable state taxes. If an estate includes high-value real estate, such as a brownstone in Brooklyn or a condo in Manhattan, crossing this tax cliff is dangerously simple. During the probate process, the executor must work alongside an expert attorney to apply every available legal deduction to pull the estate back down under the cliff edge.

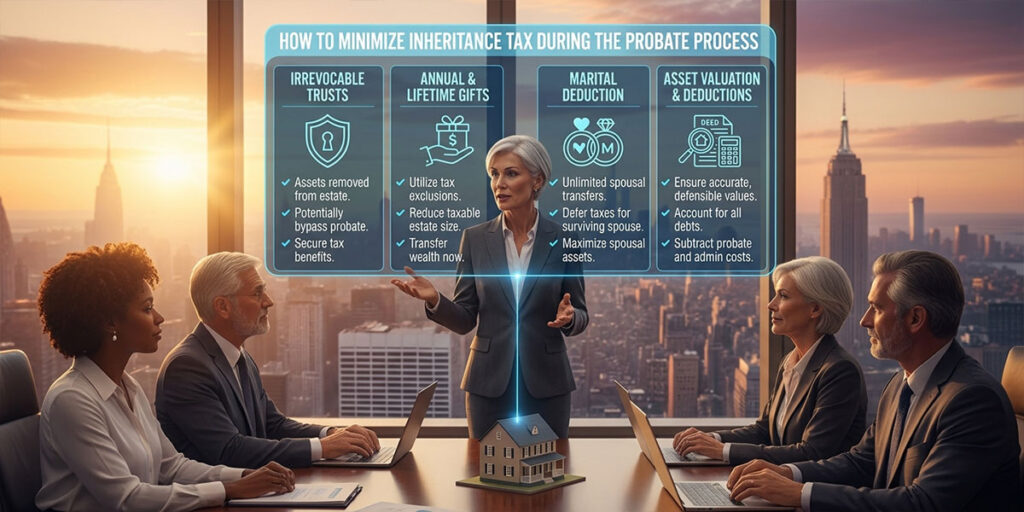

Strategic Tax Reductions Allowed During the Probate Process

Once an estate enters the formal probate system, the structural design of the assets is legally locked. However, an experienced executor can still deploy verified **New York probate tax strategies** to lower the final taxable valuation reported on the estate’s tax returns.

1. Maximizing Administrative Expense Deductions

Every dollar spent to manage, secure, and liquidate the estate can be subtracted from the total estate valuation. The executor should meticulously document and deduct the following expenses:

- Legal fees paid to your probate defense counsel.

- Appraisal costs for valuing real estate, jewelry, corporate stock, and fine art.

- Property maintenance costs, storage fees, and real estate broker commissions required to sell estate assets.

- Funeral expenses, including burial costs and memorial services.

2. Leveraging the Unlimited Marital Deduction

Under both federal tax codes and New York State statutes, any assets passing directly to a surviving spouse who is a United States citizen qualify for the Unlimited Marital Deduction. These transfers incur zero estate taxes during the current probate cycle. However, this strategy merely defers the tax burden. When the surviving spouse eventually passes away, those combined assets will face the tax cliff unless a sophisticated **trust strategy** is deployed in the meantime.

3. Utilizing Charitable Giving Deductions

If the terms of the Will direct specific funds or properties to a qualified 501(c)(3) non-profit organization, a church, or an educational institution, those allocations are fully deductible. Executors can use these charitable bequests to strategically lower the remaining estate value to sit safely below the dangerous New York tax cliff threshold.

The True Costs of Probate: Court Fees and Executor Commissions

Minimizing taxes is only half the battle. The probate process itself drains massive amounts of liquidity from an estate through statutory court fees and mandatory administrative costs. A well-developed **asset protection strategy New York** must account for these institutional leaks.

New York Surrogate’s Court Filing Fees

The state charges a sliding scale fee simply to file a probate petition. For large estates exceeding $500,000, the baseline court filing fee tops out at a fixed maximum of $1,250. While this fee is manageable, the real financial drain comes from executor commissions.

Statutory Executor Commissions

Under New York SCPA 2307, executors are legally entitled to a statutory commission for their work, calculated as a percentage of the probate estate value. The commission rates are structured as follows:

- 5.0% on the first $100,000 processed.

- 4.0% on the next $200,000 processed.

- 3.0% on the next $700,000 processed.

- 2.5% on the next $4,000,000 processed.

- 2.0% on all remaining amounts above $5,000,000.

For a $2,000,000 estate, the executor commission alone can exceed $60,000. If an estate has multiple executors, these costs can multiply. These commissions are taxable income to the executor but serve as a deduction for the estate tax return. An experienced attorney will help you calculate whether it is more financially advantageous for a family member executor to waive or accept this commission based on their personal income tax brackets.

The Premier Solution: Pre-Probate Planning to Eliminate Taxes Entirely

The ultimate strategy to **minimize estate tax New York** parameters is to bypass the probate court entirely. Assets that flow outside of the Surrogate’s Court system avoid court delays, avoid executor commissions, and can be shielded within elite trust architecture.

The Power of the Credit Shelter Trust

To protect married couples from the New York tax cliff, we often implement a Credit Shelter Trust (also known as a Bypass Trust or AB Trust). When the first spouse passes away, an amount up to the New York tax exemption limit automatically funds Trust A for the benefit of the surviving spouse. Because the assets sit inside the trust, they do not count toward the surviving spouse’s personal estate valuation. When the second spouse passes, those assets flow to the children entirely free of New York estate taxes, effectively doubling the family’s state tax protection.

Irrevocable Life Insurance Trusts (ILIT)

Life insurance payouts are generally free from ordinary income tax, but they **are included** in your gross taxable estate for estate tax calculations. If you carry a $2,000,000 policy, that death benefit could easily push your estate over the New York tax cliff. By utilizing an Irrevocable Life Insurance Trust, the trust owns the policy. The cash payout remains completely invisible to the state tax collector, allowing your heirs to use the tax-free liquidity to settle other estate expenses.

Hypothetical Scenario: The Miller Family from Manhattan

To see how these intricate mechanisms operate under pressure, consider the hypothetical case of the Miller family. Mr. Miller owned a high-value townhouse in Manhattan worth $6 million, along with $1.5 million in liquid investments. His total estate valuation stood at $7.5 million, putting him squarely over the 2026 New York estate tax cliff.

The Procrastination Failure: Mr. Miller relied on a basic, unoptimized Will. When he passed away, his executor was forced to take the estate through the heavily backlogged New York County Surrogate’s Court. Because the assets were exposed, the estate faced a massive New York estate tax bill of over $600,000, alongside $150,000 in court fees, executor commissions, and administrative delays that froze the family’s assets for 14 months.

The Morgan Legal Strategy: Had Mr. Miller engaged in **comprehensive estate planning NYC** protocols with Morgan Legal Group, our team would have restructured his real estate holdings into a Revocable Living Trust coupled with a customized Credit Shelter Trust. Upon his passing, the entire $7.5 million would have bypassed the probate process instantly. The tax mitigation clauses would have successfully eliminated the New York estate tax bill entirely, saving his children over $750,000 in unnecessary fees and taxes. Precision architecture changes everything.

Preventing Court Battles: Elite Defense Against Will Contests

High-value estates facing tax challenges are also prime targets for intra-family warfare, financial exploitation, and elder abuse. If a disgruntled relative decides to challenge the validity of a Will, the estate can be tied up in litigation for years, draining all remaining liquidity through legal defense costs.

During a live probate proceeding, our firm uses tactical legal tools to defend the estate’s integrity. If you are planning your estate proactively, we incorporate specialized “No-Contest” clauses (In Terrorem clauses) backed by strict execution standards. We ensure every document is signed in absolute accordance with New York Estates, Powers, and Trusts Law (EPTL), creating an unbreakable legal shield that deters predatory lawsuits before they can begin.

Navigating Life Changes: Incapacity and Guardianship

Tax mitigation is useless if your wealth is drained while you are still alive due to an unmanaged medical emergency. A truly well-developed estate plan addresses life, death, and everything in between.

Your asset defense structure must incorporate a statutory New York Power of Attorney and an updated Health Care Proxy. If an individual becomes incapacitated without these foundational documents, the family is plunged into a public, adversarial guardianship proceeding under Article 81 of the Mental Hygiene Law. These court battles cost tens of thousands of dollars in judicial fees—money that is directly extracted from the estate equity before you ever reach the probate phase.

Why Morgan Legal Group is the Trusted NY Authority

Defeating the aggressive tax structures of New York State requires an elite legal advocate who understands the intricate, multi-layered nature of financial defense. We do not provide cookie-cutter legal forms or basic templates.

- Decades of Battle-Tested Success: Managing over 1,000 complex estate and probate cases has given us the precise, institutional knowledge needed to navigate the Surrogate’s Court system seamlessly.

- Client-Validated Excellence: Our 900+ five-star online reviews stand as clear evidence of our transparency, deep empathy, and absolute legal accuracy.

- Nuanced Global Perspective: Led by principal attorney Russel Morgan, Esq.—a graduate of New York Law School with advanced training at LLOYD’S of London—our firm infuses international precision into domestic asset protection.

Conclusion: Secure Your Family’s Wealth Today

Minimizing taxes during the probate process requires a flawless execution of statutory deductions, meticulous fee auditing, and expert representation in front of the Surrogate’s Court judge. But the ultimate defense against the New York estate tax cliff is a proactive, well-funded trust architecture that keeps your wealth entirely out of the courtroom.

Do not leave your life’s work exposed to state mandates. Schedule an appointment with the elite team at Morgan Legal Group today. Whether you need immediate assistance navigating a current probate administration or want to construct an ironclad asset protection plan, we provide the personalized representation your legacy demands. For immediate questions, please contact us directly or discover our verified track record on our Google Business Profile. Let us build your legal fortress.

For official forms, statutory tax rates, and detailed instructions regarding estate tax filings within the state, visit the New York State Department of Taxation and Finance.

Related Resources

- How is a Will Contested in New York

- What Outcome Can Someone Expect from Probate

- Top Misconceptions About the Probate Process

- Probate Proceeding in New York

- Probate and Estate Administration in New York

- Common Challenges Faced During Probate

- Will Contests & Estate Litigation in NY

- Experience Handling Probate Matters in New York

- What Sets Our Firm Apart in Handling Probate