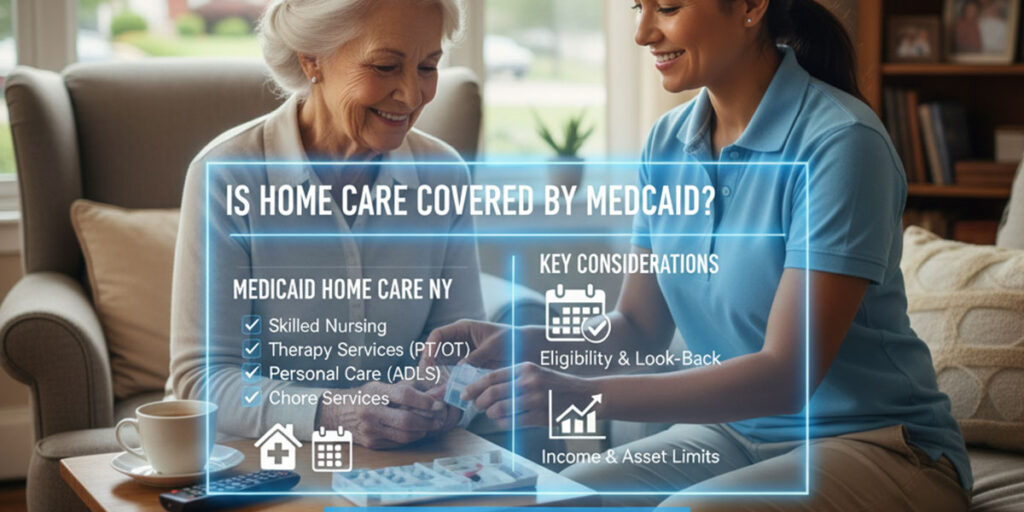

The realization that an aging loved one requires daily assistance at home often brings with it not only emotional challenges but also a significant financial shock. In New York, the cost of private home health aides frequently exceeds $6,000 to $8,000 monthly in 2026. For many families, these expenses can quickly deplete a lifetime of savings. This reality leads to a crucial question: “Does Medicaid cover home care in New York?”

The answer, fortunately, is yes. New York State’s Medicaid program offers some of the most comprehensive home-based services nationwide. However, accessing these vital benefits involves navigating complex financial criteria, strict income limits, and rigorous state review.

As the founder and lead attorney at Morgan Legal Group, I, Russel Morgan, have dedicated over 30 years to elder law and estate planning. Our firm has successfully guided more than 1,000 families through the intricacies of New York Medicaid. Our 900+ positive online reviews reflect our unwavering commitment to protecting our clients’ wealth while securing the essential care they deserve. This guide will demystify New York Community Medicaid for 2026, exploring the revolutionary CDPAP program, the impactful new look-back rules, and the precise legal strategies required to qualify without sacrificing your family’s legacy.

Navigating New York’s Home Care Landscape: Community Medicaid Explained

Before exploring the specific requirements, understanding the distinct types of Medicaid in New York is crucial. These programs operate under entirely different legal frameworks.

Community Medicaid: Supporting Care at Home

This program specifically covers home health aides who assist you in your personal residence. It allows seniors to maintain their independence and age in place with dignity. Historically, New York uniquely offered Community Medicaid without a look-back period. This meant you could transfer assets into a trust one day and apply for home care Medicaid the next. However, state legislation significantly altered this landscape for 2026.

Nursing Home Medicaid: Chronic Care Facility Coverage

In contrast, Nursing Home Medicaid pays for room, board, and medical care within a licensed nursing facility. This program maintains a stringent 5-year (60-month) “look-back” period. If you transferred assets to family members or others within five years of applying, the state will impose a severe penalty period, refusing to cover your care during that time.

The Critical Shift: New York’s Community Medicaid Look-Back Period

The most significant update for New York families in 2026 is the implementation of a look-back period for Community Medicaid. The state legislature enacted a 30-month (2.5 years) look-back period for home care services. This change fundamentally alters how families must approach planning.

Understanding the 30-Month Review

When you apply for home care services, the Department of Social Services (DSS) now meticulously audits your financial records for the 30 months immediately preceding your application. They search for “uncompensated transfers”—any assets you gave away without receiving fair market value in return. This includes significant gifts to children, transfers of property deeds, or large charitable donations.

If DSS discovers these transfers within the 30-month window, they impose a penalty period. During this period, you become solely responsible for the private cost of your home care aides. Medicaid will not cover any services until this penalty expires.

The Imperative of Proactive Planning

This rule change eliminates the possibility of “emergency Medicaid planning” for home care. You can no longer wait until a health crisis strikes to protect your assets. To build an impenetrable financial fortress, you must engage a premier elder law attorney years in advance.

Meeting Medicaid’s Financial Benchmarks: Income and Asset Limits

Medicaid functions as a means-tested program, designed to assist those with limited financial resources. To qualify in New York, you must demonstrate that your income and total assets fall below specific, strict limits established by the Department of Health.

2026 Asset Thresholds for Community Medicaid

An individual applying for Community Medicaid can retain only a very modest amount of liquid assets, such as cash, stocks, or non-exempt property. In 2026, this limit is approximately $31,175. For married couples where both spouses require care, the combined limit rises to approximately $42,312. If your savings exceed these figures, you face an “excess assets” challenge, requiring strategic repositioning of funds before you submit your application.

2026 Income Thresholds for Community Medicaid

The income limits prove equally restrictive. An individual applicant may keep approximately $1,732 per month in income from sources like Social Security or pensions. If your monthly income surpasses this amount, you have “excess income.” Historically, the state required you to spend this excess on medical care each month before Medicaid would cover home health aides. Fortunately, New York provides an effective legal solution to this common problem.

Strategic Solutions for Medicaid Qualification: Trusts That Protect

When your income or assets exceed Medicaid’s strict limits, specialized legal tools can help you qualify without depleting your life savings.

The Pooled Income Trust: Managing Excess Income

If your monthly income exceeds the Medicaid threshold, you do not have to endure financial hardship. A Pooled Income Trust, authorized by both federal and state law, offers a brilliant solution. Managed by a non-profit organization, this trust allows you to deposit your “excess income” each month. For example, if you have $1,268 in excess income, depositing this amount into the trust means Medicaid no longer counts it as your income, making you instantly eligible for full home care coverage. You retain access to these funds; the non-profit uses them to pay your ongoing living expenses, such as rent, property taxes, utilities, or groceries. This trust effectively transforms disqualifying income into permissible living expenses.

The Medicaid Asset Protection Trust (MAPT): Safeguarding Your Wealth

What if you own a valuable home or significant investments? A Pooled Income Trust cannot hold these substantial assets. To qualify for Medicaid and protect your family’s inheritance, you need a Medicaid Asset Protection Trust (MAPT). Our legal team establishes this irrevocable trust, naming someone else, typically your adult children, as Trustees. You then transfer the deed to your house and your excess bank accounts into the Trust.

Because the MAPT is irrevocable, and you no longer legally own these transferred assets, Medicaid cannot count them against your asset limit. You can continue living in your home for life, and the Trust shields it from Medicaid Estate Recovery liens after your passing, ensuring it transfers safely to your heirs, bypassing the probate process.

Crucial Warning: Transferring assets into a MAPT triggers the 30-month look-back period for home care and the 60-month look-back period for nursing homes. This underscores why you must implement this strategy while you are still healthy and well in advance of needing care.

Empowering Your Care Choices: New York’s CDPAP Program

One of the most innovative and patient-centric features of New York’s Community Medicaid system is the Consumer Directed Personal Assistance Program (CDPAP). This program offers unparalleled flexibility and control over your home care.

Beyond Traditional Agency Models

Under standard Medicaid home care, the state assigns a home health aide from an approved agency. This model often leaves patients with limited input on who provides their care, potentially leading to challenges like language barriers, scheduling difficulties, or high caregiver turnover.

The CDPAP Advantage: Directing Your Own Care

CDPAP revolutionizes this by empowering the patient to hire their own caregivers. If you qualify for Medicaid home care, you gain the freedom to select a trusted individual—your daughter, son, a close friend, or a neighbor—as your caregiver. You effectively become the employer. The state pays your chosen caregiver an hourly wage directly through a fiscal intermediary. This program not only ensures you receive care from someone you know and trust but also provides a legitimate income for family members who may have left their jobs to care for you, honoring their dedication.

Who Cannot Be Hired Under CDPAP?

While CDPAP offers broad flexibility, certain restrictions apply. You cannot hire your legal spouse. Additionally, you cannot hire your “designated representative,” who manages the CDPAP paperwork on your behalf if you lack the cognitive ability to do so.

A Unique New York Protection: Spousal Refusal

Medicaid typically views a married couple as a single financial unit. If one spouse requires home care, Medicaid considers the income and assets of both individuals. Should the “well spouse” (or community spouse) possess substantial wealth, the “sick spouse” could face a denial of coverage. New York stands as one of the very few states that honors the legal concept known as Spousal Refusal.

Executing a Spousal Refusal

If the well spouse formally refuses to contribute their assets towards the care of the sick spouse, they can sign a specific “Spousal Refusal” document. Under New York law, Medicaid must then disregard the well spouse’s assets and evaluate the sick spouse’s eligibility as a single individual. This crucial protection allows the sick spouse to obtain immediate home care coverage.

Important Considerations and Legal Defense

While Spousal Refusal secures immediate care, Medicaid retains the right to pursue the well spouse later for “support.” Navigating a Spousal Refusal demands aggressive legal representation to effectively negotiate with the state and protect the family’s overall financial security from potential subsequent lawsuits.