Which Assets Go Through Probate in New York? (2026 Guide): The Definitive List of Probate vs. Non-Probate Property

The loss of a loved one brings immense grief. Navigating their estate should not add to that burden. Yet, many New York families face an unexpected challenge: discovering that assets they believed were easily accessible are "frozen" by the court system. This often happens due to a fundamental misunderstanding of New York probate. Probate is the legal process that validates a Will and oversees the distribution of a deceased person’s property.

At Morgan Legal Group, we frequently guide clients through the complexities of New York Surrogate’s Court. Our experience, spanning decades and thousands of estate cases, reveals a consistent truth: whether an asset becomes entangled in probate depends entirely on how it was titled at the time of death. This guide aims to demystify the process. We clearly distinguish between assets that require probate and those designed to bypass it, empowering you to protect your family’s legacy.

Understanding New York Probate: The Core Principle

New York probate is the judicial process where a Surrogate’s Court validates a deceased person’s Will (or determines heirship if no Will exists) and formally authorizes an Executor or Administrator to manage and distribute their estate. This court oversight ensures that debts are paid, and remaining assets are transferred to the rightful beneficiaries or heirs according to the Will or state law.

The crucial factor determining whether an asset enters this process is its ownership structure. Generally, any asset held solely in the deceased individual’s name, without a designated beneficiary or joint owner, must pass through probate. If an asset has no automatic legal path to a new owner, the court must provide one.

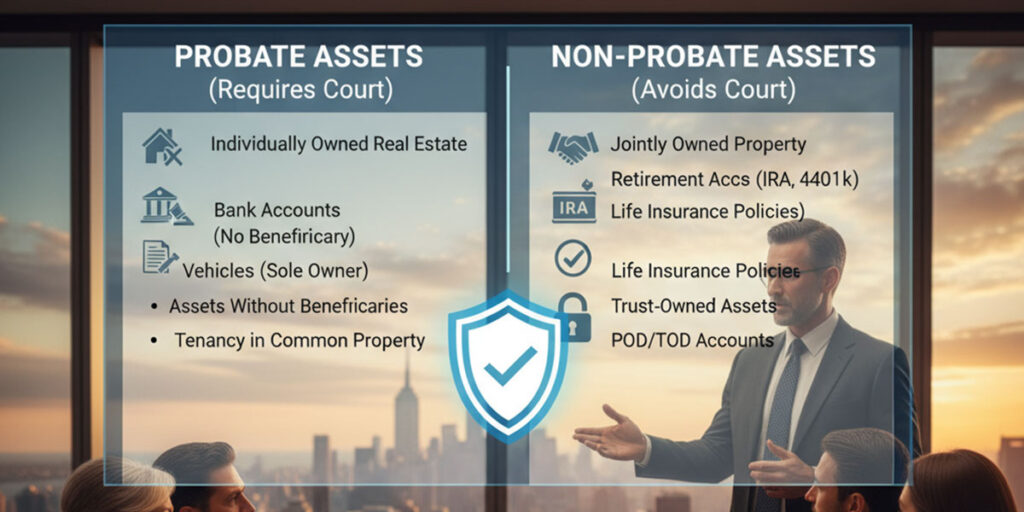

Assets That Typically Require New York Probate

Many assets, if not properly structured, become "probate assets" – meaning they cannot be transferred without court intervention. Understanding these categories is the first step toward proactive estate planning.

Real Estate Owned Individually

For many New Yorkers, real estate represents the most significant asset. Its probate status hinges entirely on how the deed is worded.

- Sole Ownership: A property titled simply in "John Doe’s name" will require probate for its transfer. An Executor must be appointed by the Surrogate’s Court before the property can be sold, refinanced, or formally transferred to heirs.

- Tenants in Common (TIC): This ownership structure is common among unmarried partners or siblings. If a deed lists "John Doe and Jane Smith" without specifying "joint tenants," New York law presumes a Tenancy in Common. Upon John’s death, his share (e.g., 50%) does not automatically transfer to Jane. Instead, it becomes part of his probate estate, requiring court action to transfer to his designated heirs. Jane then co-owns the property with John’s heirs.

Bank and Investment Accounts Without Beneficiaries

Financial accounts are frequently frozen upon notification of death, causing immediate financial strain for surviving family members.

- Individual Checking/Savings Accounts: Any account solely in the deceased’s name is typically frozen. Even if a Will specifies who should receive the funds, banks generally require Letters Testamentary (or Letters of Administration) from the court to release them.

- Brokerage Accounts Lacking POD/TOD Designations: Stocks, bonds, and other investments held in an individual’s name without a "Transfer on Death" (TOD) or "Payable on Death" (POD) designation are probate assets. Their transfer requires court authorization.

- Checks Payable to the Deceased: Final paychecks, tax refunds, or other checks made out to the decedent cannot be cashed by family members. These funds must be deposited into an "Estate Account," which can only be opened after an Executor or Administrator is appointed through probate.

Tangible Personal Property

While often distributed informally, valuable personal items technically fall under probate if not specifically addressed.

- Valuables and Collectibles: Art collections, jewelry, antiques, and other significant personal property are considered probate assets unless they are specifically held within a trust.

- Automobiles: Cars titled solely in the deceased’s name are probate assets. While the New York Department of Motor Vehicles offers a simplified process for transferring one vehicle to a surviving spouse or child without full probate, this is typically limited by value and specific circumstances.

Business Interests Not Structured for Succession

For entrepreneurs and business owners in New York, proper estate planning is crucial. Without it, business interests can become frozen, jeopardizing operations and value.

- Sole Proprietorships: A business operating as a sole proprietorship is legally inseparable from its owner. Upon the owner’s death, the business’s assets (equipment, inventory, receivables) become part of the probate estate.

- LLC Membership Interests & Corporate Shares: Unless an LLC operating agreement or corporate bylaws contain specific provisions for transfer upon death, membership interests or privately held corporate shares are probate assets. This can leave a business without authorized leadership to manage payroll, contracts, or daily operations until an Executor is appointed.

Life Insurance and Retirement Accounts with Flawed Beneficiary Designations

These "contract assets" are designed to bypass probate, but common mistakes can inadvertently pull them into the court system.

- Naming "My Estate" as Beneficiary: If you designate "My Estate" as the beneficiary for a life insurance policy or retirement account (e.g., 401(k), IRA), these funds will be paid to your estate, triggering probate.

- No Living Beneficiary: Failing to name any beneficiary, or not updating beneficiaries after a primary beneficiary has passed away, means the asset will default to your estate and require probate for distribution.

Assets That Often Bypass Probate in New York

Strategic planning allows many assets to transfer directly to your chosen beneficiaries without court involvement, saving time, expense, and stress for your loved ones.

Jointly Owned Real Estate with Survivorship Rights

Certain forms of joint property ownership ensure a seamless transfer.

- Joint Tenants with Right of Survivorship (JTWROS): If a deed explicitly states "Joint Tenants" or "Joint Tenants with Right of Survivorship," the deceased owner’s share automatically transfers to the surviving joint owner(s) upon death, outside of probate.

- Tenants by the Entirety: This specialized form of joint ownership is exclusively for married couples in New York. It functions similarly to JTWROS, guaranteeing the surviving spouse automatically inherits the property without probate upon the first spouse’s death.

Financial Accounts with Designated Beneficiaries

Properly designating beneficiaries on financial accounts is a straightforward way to avoid probate.

- Payable on Death (POD) / Transfer on Death (TOD) Accounts: By completing a POD form at your bank or a TOD form for your brokerage account, you name a beneficiary who will receive the funds directly upon your death, bypassing probate entirely.

- Joint Accounts with Survivorship: Most joint bank accounts in New York are established with a "right of survivorship." The surviving account holder gains full ownership immediately upon the death of the other joint owner.

Life Insurance and Retirement Accounts with Valid Beneficiaries

When correctly structured, these assets are powerful probate-avoidance tools.

- Named Living Beneficiaries: If you designate a specific living individual (or individuals) as the beneficiary of your life insurance policy or retirement account, the funds are paid directly to them by the institution, outside of the probate process. It is vital to review and update these designations regularly.

Assets Held Within a Revocable Living Trust

A Revocable Living Trust is a comprehensive estate planning tool specifically designed to keep assets out of probate.

When you establish a Revocable Living Trust, you transfer ownership of your assets (real estate, bank accounts, investments, business interests) from your individual name into the name of the Trust (e.g., "John Doe, Trustee of the Doe Family Trust"). Because the Trust, not you individually, "owns" the assets, and a Trust does not "die," these assets avoid probate. Upon your passing, your designated Successor Trustee simply steps in to manage and distribute the assets according to your instructions, without court approval.

New York’s Small Estate Exception: Voluntary Administration

New York law offers a simplified process for very small estates, known as Voluntary Administration (or "Small Estate" proceeding) under Article 13 of the Surrogate’s Court Procedure Act.

If the total value of all probate assets (assets solely in the deceased’s name without beneficiaries) is less than $50,000 (excluding one vehicle), your family might qualify for this expedited process. It is generally faster and less costly than full probate. However, it’s crucial to note that real estate often disqualifies an estate from using the Small Estate proceeding, even if the total personal property value is below the threshold. The Surrogate’s Court website offers valuable resources on this process.

Protecting Your Legacy: The Power of Proactive Estate Planning

The distinction between probate and non-probate assets highlights a critical truth: probate is often a choice, not an inevitability. By understanding how your assets are titled and utilizing effective estate planning strategies, you can spare your family the delays, costs, and emotional strain associated with court-supervised asset distribution.

Whether through careful beneficiary designations, joint ownership, or the establishment of a Revocable Living Trust, you have the power to direct your legacy efficiently and privately. This proactive approach ensures your wishes are honored and your loved ones receive their inheritance without unnecessary obstacles.

Summary: New York Probate Assets at a Glance

To provide clarity, here’s a quick overview of common asset types and their typical probate status:

| Asset Type | Typically Probate? | How to Avoid Probate |

|---|---|---|

| Real Estate (Sole Name) | YES | Joint Tenants, Tenants by Entirety, Life Estate, Trust |

| Real Estate (Tenants in Common) | YES | Convert to JTWROS, Life Estate, Trust |

| Bank Accounts (Sole Name) | YES | POD/TOD designation, Joint Account, Trust |

| Brokerage Accounts (No POD/TOD) | YES | TOD designation, Trust |

| Life Insurance (Beneficiary: "Estate" or None) | YES | Name living beneficiary, Trust |

| Retirement Accounts (Beneficiary: "Estate" or None) | YES | Name living beneficiary, Trust |

| Business Interests (Sole Prop, Unstructured LLC/Corp) | YES | Operating Agreement, Buy-Sell Agreement

|