The realization that an aging parent or spouse requires daily assistance is a difficult emotional milestone. This realization is almost immediately followed by a severe financial shock. In 2026, the cost of private home health aides in New York State frequently exceeds $6,000 to $8,000 per month. For most middle-class families, paying out-of-pocket for round-the-clock care will drain a lifetime of savings in a matter of months.

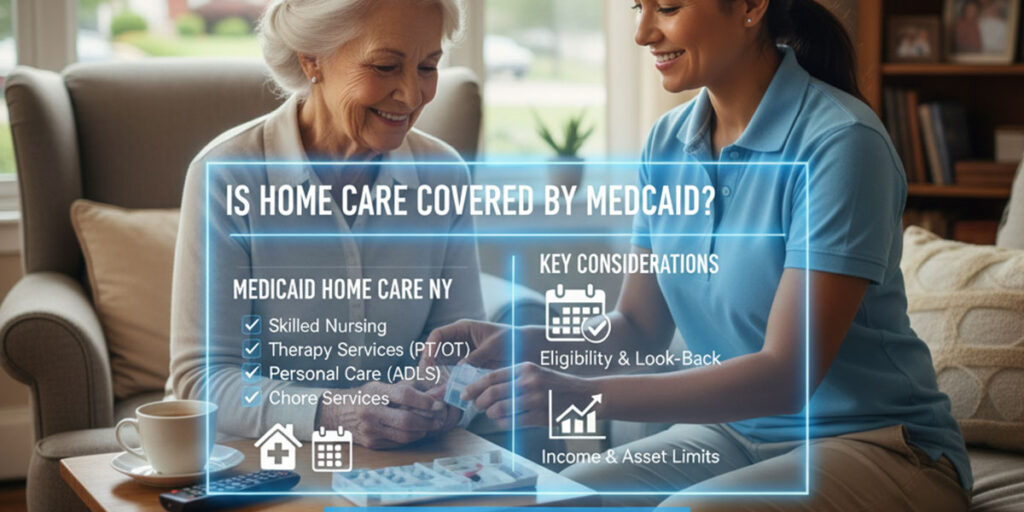

Families inevitably ask a desperate question: Does Medicaid cover home care?

The short answer in New York is yes. The New York State Medicaid program is actually one of the most robust in the entire country regarding home-based services. However, the long answer is fraught with complex financial hurdles, strict income limits, and aggressive state scrutiny.

I am Russel Morgan, the founder and lead attorney at Morgan Legal Group. For over 30 years, our firm has specialized exclusively in elder law and estate planning. We have successfully guided over 1,000 families through the New York Medicaid labyrinth. Our 900+ positive online reviews reflect our unwavering commitment to protecting our clients’ wealth while securing the vital care they deserve.

In this comprehensive cornerstone guide, we will demystify Community Medicaid in New York for 2026. We will explore the revolutionary CDPAP program, the devastating new look-back rules, and the precise legal trusts required to qualify without losing your family home.

1. Understanding the Difference: Community Medicaid vs. Nursing Home Medicaid

Before diving into the rules, you must understand the two distinct branches of the New York Medicaid system. They operate under entirely different legal frameworks.

Nursing Home Medicaid (Chronic Care)

This program pays for room, board, and medical care inside a licensed nursing facility. It is notoriously strict. It features a rigid 5-year (60-month) “look-back” period. If you transferred any assets to your children within five years of applying, the state will hit you with a severe penalty period, refusing to pay for your care.

Community Medicaid (Home Care)

This is the program that pays for home health aides to come to your personal residence. It allows seniors to age in place with dignity. Historically, New York was unique because Community Medicaid had no look-back period. You could transfer your wealth to a Trust on Monday and apply for home care Medicaid on Tuesday. Unfortunately, state legislation has drastically altered this landscape for 2026.

2. The New York Community Medicaid Look-Back Period

The most critical update for New York families in 2026 is the implementation of the Community Medicaid look-back period. The state legislature enacted a 30-month (2.5 years) look-back period for home care services.

How the 30-Month Rule Works

When you apply for home care services, the Department of Social Services (DSS) will now audit your financial records for the preceding 30 months. They are searching for uncompensated transfers. Did you give your daughter $50,000? Did you transfer the deed of your Brooklyn house to your son? Did you make large charitable donations?

If they discover these transfers within the 30-month window, they will impose a penalty period. During this penalty period, you are fully responsible for paying the private cost of your home care aides. Medicaid will not cover a single hour until the penalty expires.

The Necessity of Proactive Planning

This rule change destroys the concept of “emergency Medicaid planning” for home care. You can no longer wait until you get sick to protect your assets. You must engage a premier elder law attorney years in advance to build an impenetrable financial fortress.

3. The Financial Thresholds: Can You Afford to Be Poor?

Medicaid is a means-tested program. It is designed for the impoverished. To qualify in New York, you must prove that your income and your total assets fall below strict, highly specific limits set by the Department of Health.

The 2026 Asset Limits

An individual applying for Community Medicaid is permitted to keep only a very small amount of liquid assets (cash, stocks, non-exempt property). In 2026, this limit is approximately $31,175. If you are a married couple and both need care, the limit is approximately $42,312.

If you have $100,000 in a savings account, you do not qualify. You have a “spend-down” problem. You must legally reposition that excess $68,825 before submitting your application.

The 2026 Income Limits

The income limits are equally restrictive. An individual applicant is allowed to keep approximately $1,732 per month in income (Social Security, pensions). If your monthly income is $3,000, you have $1,268 of “excess income.”

Historically, the state required you to spend that excess $1,268 on medical care every single month before Medicaid would pay for your home health aides. Fortunately, New York offers a brilliant legal loophole to solve this exact problem.

4. Solving the Income Problem: The Pooled Income Trust

If your monthly income exceeds the strict Medicaid limits, you do not have to live in poverty. You can utilize a legal structure authorized by both federal and state law: The Pooled Income Trust.

How the Pooled Trust Operates

A Pooled Income Trust is managed by a non-profit organization. When we set up this trust for our clients, we instruct them to deposit their “excess income” into the trust account every month.

For example, if you have $1,268 in excess income, you deposit that exact amount into the Pooled Trust. Because the money is inside the trust, Medicaid no longer counts it as your income. You instantly qualify for full home care coverage.

Spending Your Money

You do not lose the money you put into the Pooled Trust. The non-profit organization uses those funds to pay your living expenses. They will use your $1,268 to pay your rent, your property taxes, your utility bills, or your grocery bills. The Pooled Trust acts as a legal filter, transforming “disqualifying income” into “permissible living expenses.”

5. Solving the Asset Problem: The Medicaid Asset Protection Trust (MAPT)

What if you own a home in Queens worth $1.2 million? What if you have $400,000 in a brokerage account? You cannot put these assets into a Pooled Income Trust. To qualify for Medicaid and protect your family’s inheritance, you must utilize a Medicaid Asset Protection Trust (MAPT).

The Irrevocable Nature of the MAPT

A MAPT is an irrevocable trust. You work with our legal team to establish the trust, and you name someone else (usually your adult children) as the Trustees. You then transfer the deed to your house and your excess bank accounts into the Trust.

The Shield Effect

Because the trust is irrevocable and you no longer own the assets, Medicaid cannot count them against your $31,175 asset limit. You can live in your house for the rest of your life. The Trust protects the house from Medicaid Estate Recovery liens after you die. The house transfers safely to your children, bypassing the probate process entirely.

Crucial Warning: Transferring assets into a MAPT triggers the 30-month look-back period for home care and the 60-month look-back period for nursing homes. This is why you must execute this strategy while you are still healthy.

6. The CDPAP Program: Hiring Your Own Family

One of the most remarkable features of New York’s Community Medicaid system is the Consumer Directed Personal Assistance Program (CDPAP).

The Traditional Agency Model

Under standard Medicaid home care, the state assigns a home health aide from an approved agency. You have little control over who walks into your home. You may face language barriers, scheduling conflicts, or high turnover rates.

The CDPAP Revolution

CDPAP completely shifts the power to the patient. If you qualify for Medicaid home care, CDPAP allows you to hire your own caregivers. You can hire your daughter, your son, a trusted neighbor, or a close friend. You become the employer.

The state pays the caregiver an hourly wage directly through a fiscal intermediary. This allows adult children who have quit their jobs to care for aging parents to receive a legitimate income. It ensures the patient receives care from someone who genuinely loves them and understands their unique cultural or medical needs.

Who Cannot Be Hired Under CDPAP?

The rules are broad, but there are exceptions. You cannot hire your legal spouse. You also cannot hire your “designated representative”—the person who manages the CDPAP paperwork on your behalf if you lack the cognitive ability to do so.

7. Spousal Refusal: New York’s Unique Protection

Medicaid views a married couple as a single financial unit. If a husband needs home care, Medicaid will look at the wife’s income and assets. If the “well spouse” (the community spouse) has significant wealth, the “sick spouse” will be denied coverage.

New York is one of the very few states that honors a legal concept called Spousal Refusal.

Executing the Refusal

If the well spouse refuses to contribute their assets to the care of the sick spouse, they can sign a formal “Spousal Refusal” document. Under New York law, Medicaid must then ignore the well spouse’s assets and evaluate the sick spouse as a single individual.

The Caveat

This allows the sick spouse to get immediate home care. However, Medicaid retains the right to sue the well spouse later for “support.” Navigating a Spousal Refusal requires aggressive legal representation to negotiate with the state and protect the family’s overall wealth from these subsequent lawsuits.

8. The Application Process: A Bureaucratic Minefield

Applying for Community Medicaid in New York is not like applying for a driver’s license. It is a rigorous, adversarial legal proceeding.

The Document Audit

The Department of Social Services will demand years of financial records. They will scrutinize every bank statement, tax return, property deed, and life insurance policy. If a single $500 check is unexplained, they will delay or deny the application.

The Medical Assessment

Beyond the financial audit, you must pass a medical assessment. A nurse sent by a Conflict-Free Evaluation and Enrollment Center (CFEEC) will evaluate your daily needs. They determine how many hours of home care you actually require. If you do not advocate for yourself properly, they may authorize only four hours a day when you desperately need twelve.

9. Case Study: Rescuing Robert in Brooklyn

To illustrate the power of expert legal counsel, let us examine a hypothetical scenario based on common cases we resolve at Morgan Legal Group.

Meet Robert. He is an 80-year-old widower living in Brooklyn. He suffers from advanced Parkinson’s disease. He needs a home health aide 12 hours a day. Private care would cost him $7,000 a month. Robert’s sole income is a $2,500 monthly pension. He owns his Brooklyn brownstone outright (worth $1.5 million) and has $50,000 in savings.

The DIY Disaster

Robert’s son tries to apply for Medicaid online. The state instantly denies Robert. His income is too high, his savings are too high, and his house exposes him to future estate recovery.

The Morgan Legal Group Strategy

Robert’s son hires our firm. We immediately implement a multi-tiered defense:

- We establish a Pooled Income Trust for Robert’s excess $768 monthly income, securing his income eligibility.

- We draft an irrevocable Medicaid Asset Protection Trust and transfer the deed to the brownstone, shielding the $1.5 million asset.

- We legally “spend down” the excess $50,000 in savings by prepaying funeral expenses and making permissible home modifications.

- We guide Robert through the medical evaluation, securing approval for the CDPAP program.

The Result: Robert remains in his beloved Brooklyn home. His son acts as his paid caregiver through CDPAP. Robert pays zero out-of-pocket for his care. Upon his passing, the brownstone transfers to his son completely tax-free and untouched by the government.

10. Why You Must Hire a Premier Elder Law Attorney

The rules governing Medicaid, guardianships, and trusts are arguably the most complex in all of New York jurisprudence. A single mistake—transferring a deed incorrectly, failing to explain a bank withdrawal, or filling out a Pooled Trust joinder agreement wrong—will result in catastrophic financial loss.

At Morgan Legal Group, we do not view Medicaid planning as a simple paperwork exercise. We view it as high-stakes asset protection. We interface directly with the Department of Social Services, shielding our clients from bureaucratic harassment.

If you suspect a loved one is being financially manipulated during this vulnerable time, our elite litigators have deep experience exposing elder abuse and recovering stolen assets before the Medicaid application is filed.

Conclusion: Act Before the Look-Back Traps You

Does Medicaid cover home care in New York? Yes. It is an incredible resource that allows seniors to age safely in their own homes. Programs like CDPAP provide unmatched flexibility and comfort.

However, the 2026 introduction of the 30-month look-back period changes everything. You can no longer afford to wait until a health crisis strikes. You must engineer your estate plan today to ensure you qualify for care tomorrow.

Protect your life’s work and secure your care. Schedule a consultation with Morgan Legal Group immediately. We will audit your assets, design a customized MAPT, and guide you flawlessly through the Medicaid maze. For urgent assistance with an impending home care crisis, please contact us directly. We are ready to stand as your ultimate legal shield.

For official information regarding the income limits and programmatic rules of the state Medicaid system, please review the resources provided by the New York State Department of Health (DOH).